Evergreen funds: Balancing access, returns and liquidity

About evergreen funds

- Evergreen funds, also known as semi-liquid funds, raise capital on an ongoing basis and offer investors liquidity at stated intervals—typically monthly, quarterly, or semiannually.

- These structures seek to provide investors access to illiquid private market asset classes spanning private credit, private equity, real estate, and infrastructure.

- These funds’ liquidity mechanisms are designed to balance the longer‑duration nature of private market investments with opportunities for periodic investor liquidity.

The rise of evergreen funds

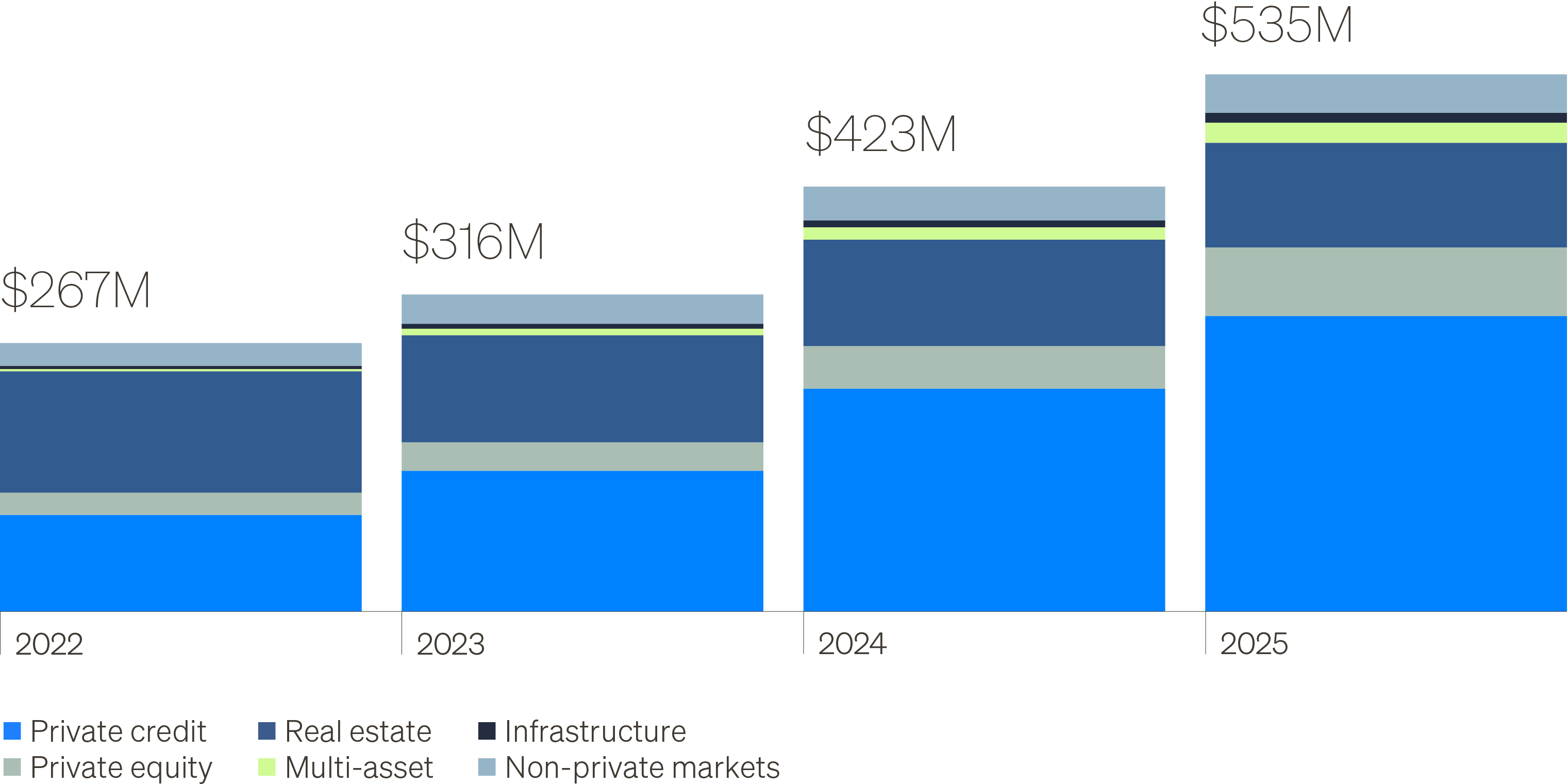

Evergreen funds have grown rapidly in recent years, evolving from a niche private markets vehicle aimed primarily at retail investors to a broader access point across the wealth and institutional landscape. Asset in these vehicles topped $530 billion in 2025, roughly double their level three years earlier, with private credit accounting for the largest share of assets, followed by real estate and private equity.1 As investors increasingly turn to evergreen funds for private markets exposure in more investor‑friendly vehicles, the opportunity set must be weighed against key considerations around liquidity, fees and fund structure.

U.S. Evergreen fund AUM by strategy

Return premium

Evergreen funds often allocate the majority of their portfolios to illiquid assets, such as private equity, private credit, real estate, and infrastructure. Private assets lack the inherent liquidity of public markets. They trade in less active markets, where transactions are negotiated and buyers can be limited. That means liquidity is intermittent, and exiting an investment often comes down to finding a buyer, rather than being able to sell quickly at a quoted market price. In exchange for reduced liquidity, investors may be compensated with potentially higher returns—commonly referred to as the “illiquidity premium.” Therefore, evergreen funds may work well for investment strategies that require a long-term investment horizon while still allowing investors to sell their shares at defined intervals.

Shareholder liquidity

While evergreen funds offer more liquidity than traditional private market drawdown funds, they remain less liquid than publicly traded securities, mutual funds and ETFs. Rather than offering daily access, evergreen funds provide periodic liquidity by offering to repurchase shares at set intervals, such as monthly, quarterly or semiannually. Repurchase amounts vary by fund but are commonly capped at a set percentage of net asset value (NAV), typically 5% per quarter. These limitations are structural and intentional to manage liquidity prudently, limiting the need to sell less liquid or illiquid assets during volatile markets and helping protect remaining investors from dilution or adverse pricing.

If redemption requests exceed the amount the fund has offered to repurchase, investors may receive only a portion of their requested amount. In these cases, shareholders are typically treated equally, with redemptions fulfilled on a pro rata basis—meaning each investor receives the same percentage of their request.

Best practices for fund management

Manager selection is critical in private markets, where outcomes are highly dependent on sourcing, underwriting and portfolio management. This is especially important in evergreen structures, where managers must also thoughtfully manage capital flows and periodic liquidity.

When evaluating evergreen funds, investors should focus on three key indicators of effective management:

- Disciplined liquidity management Maintain reserves of cash, liquid credit instruments and available credit lines to meet redemptions without negatively impacting long-term returns.

- Thoughtful portfolio construction Build diversified portfolios to avoid concentration risk and include investments that produce cash flow overtime (i.e., interest income, maturing assets, exits)

- Robust valuation practices Apply rigorous valuation practices to ensure NAVs accurately reflect the portfolio’s fair value, incorporating independent third-party valuations as appropriate.

Comparison of evergreen fund structures

Evergreen funds represent a thoughtful evolution in private market investing. By understanding their structure, benefits and liquidity features, investors can confidently pursue strategies that align with their long-term investment goals while maintaining access to periodic liquidity.

Summary

Evergreen funds may help address many of the historical challenges for individuals to access the yield, return and diversification potential of private market investing. As with any investment decision, investors should consider the investment risks, expertise of managers and their ability to execute their strategy using different investment structures.