Why the Fed is likely to cut rates

Given all of the uncertainty caused by a dramatic ramp-up in U.S. tariffs, an economy that has gradually weakened while simultaneously on pins and needles over any real or imagined near-term inflation increase, and the potential politicization of any future Fed decisions, we understand why it has taken markets and many market commentators time to catch up to what is now almost inevitable: The Fed cutting rates by 50bps–75bps by the end of the year for economic reasons, not political ones (and given the recent payroll revisions, there is certainly a possibility that they go by 100bps by year end).

Since the upcoming Fed meeting is almost upon us, I thought it made sense to share with you the framework we have been using to better understand why the Fed should cut, and will cut, despite the potential for stickier near-term inflation.

We don’t have the conditions to set off sustained inflation

Tariffs are a tax: Hence, the Congressional Budget Office’s (CBO’s) $3.3 trillion revenue estimate for the Treasury. So let’s call that $300 to $330 billion per year going to the U.S. government that will not go to: a) our trading partners, b) corporate America to hire more workers or invest in growth and c) consumers to do what they do best: CONSUME!

By definition, this is fiscally contractionary. The economy is still in solid shape, but the labor market has evolved from white hot several years ago to somewhere in the warm to cool range (withholding tax collections would argue for warm, total job creation would say cool).

Yes, tariffs will boost near-term inflation numbers; however, we do not have the necessary and sufficient conditions to set off another sustained period of inflation. As a reminder, the previous period of inflation was primarily caused by:

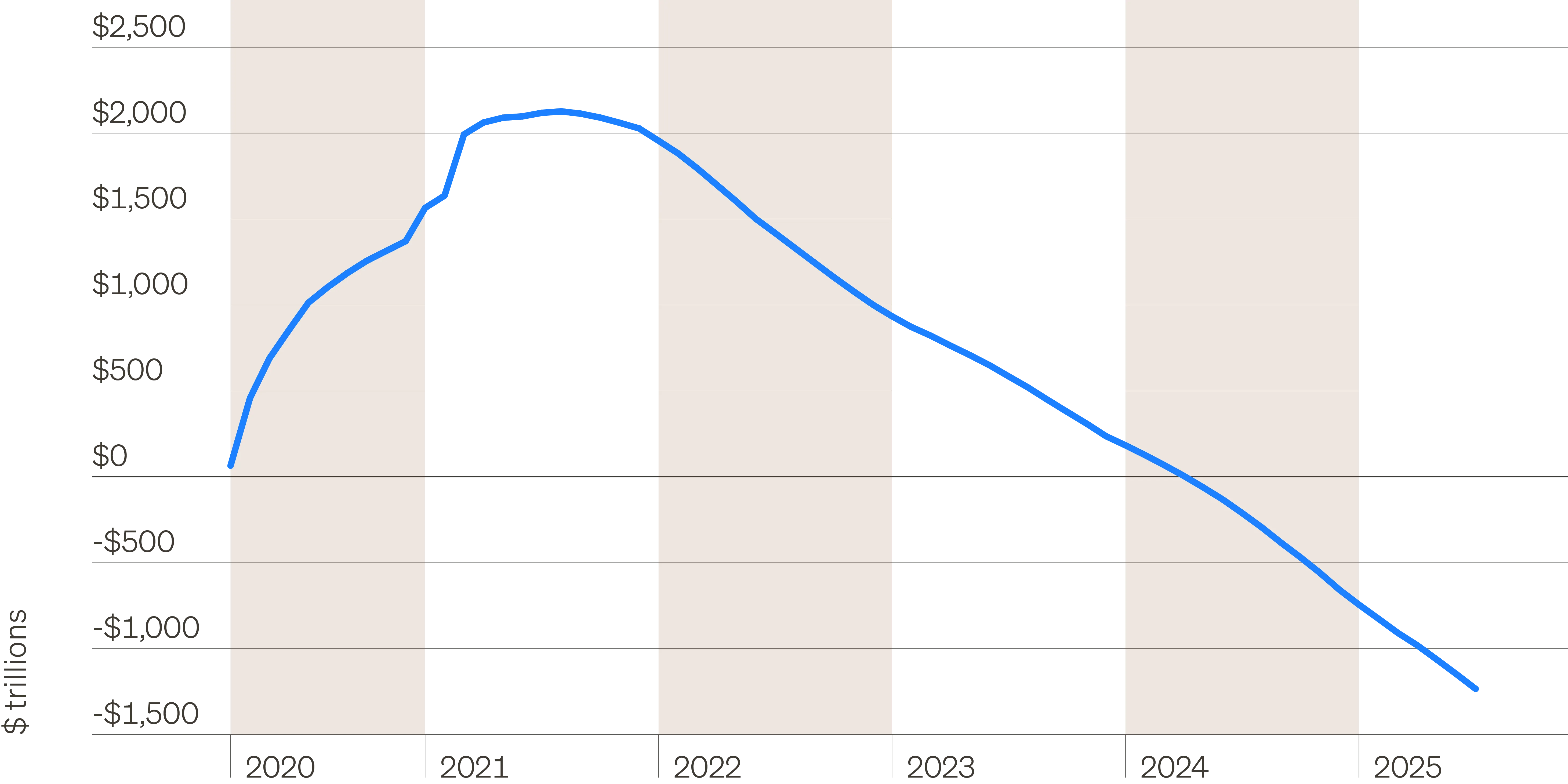

- Money supply: 42% growth in money supply in two years (see chart below, “Relative to nominal GDP v M21 money supply”)

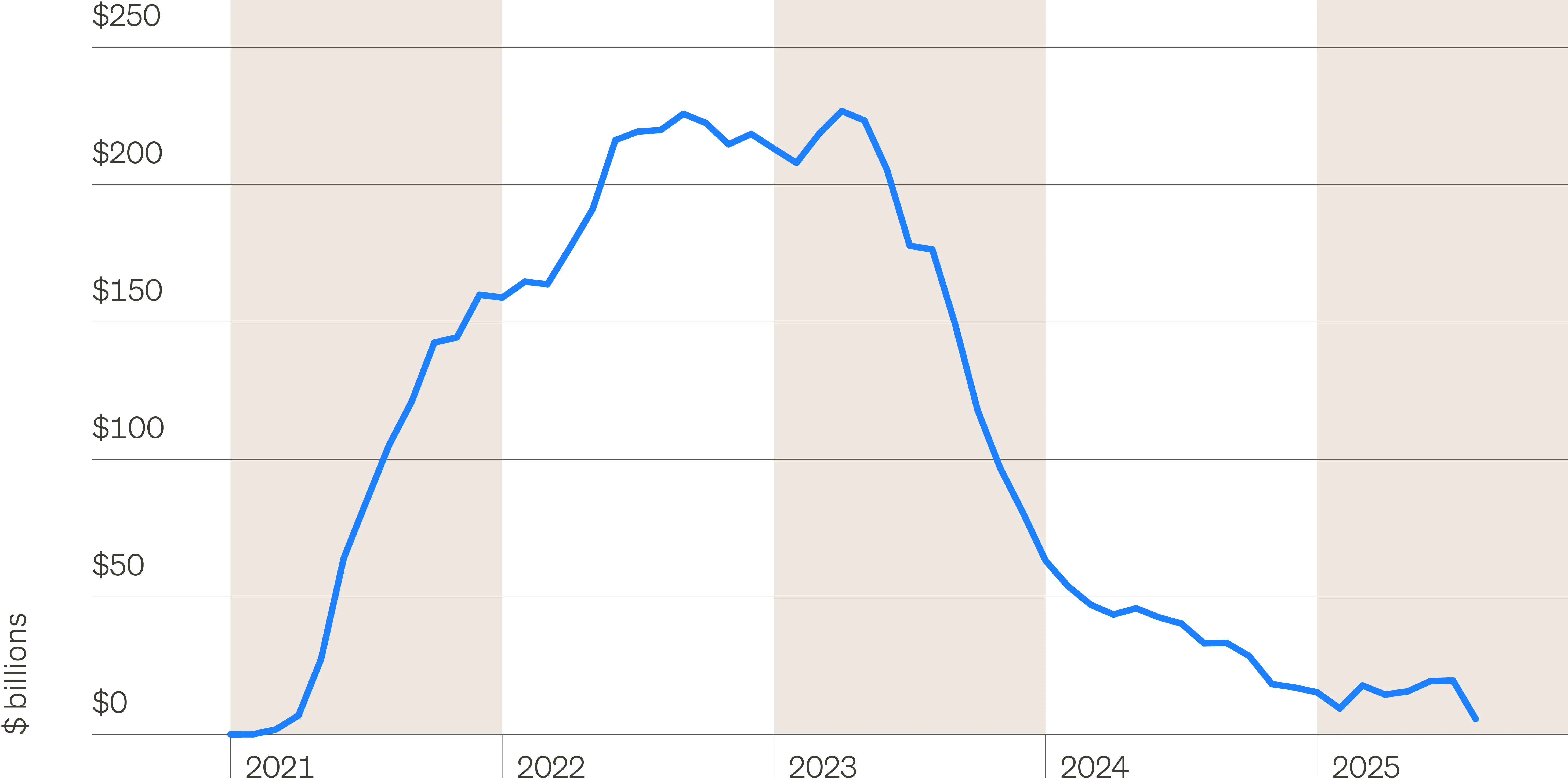

- Savings: Transfer payments to consumers that boosted excess savings by $2 TR (see chart “Excess savings post 2020 recession”).

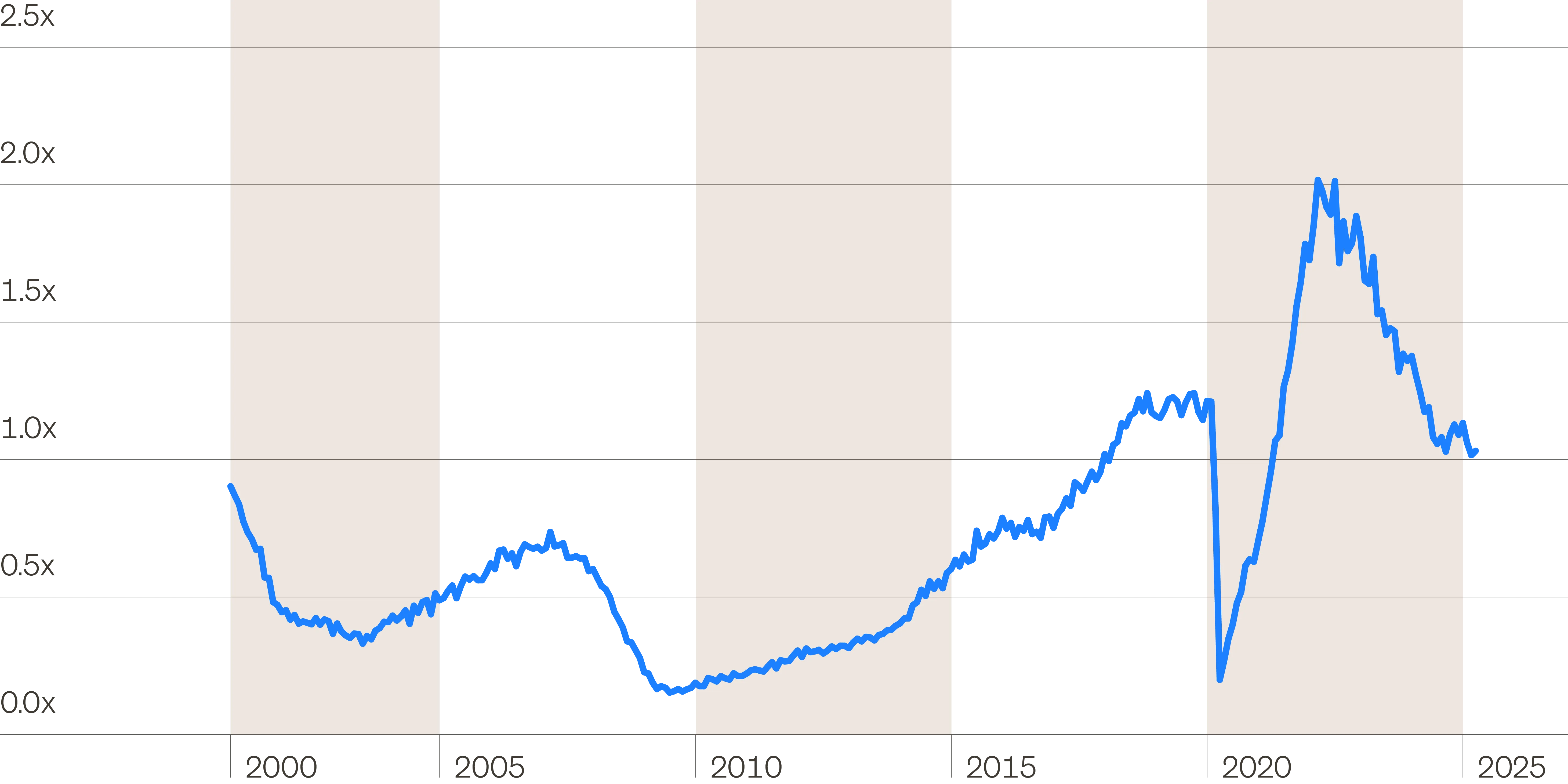

- Labor market: Exacerbated by a white hot labor market with two job opening per unemployed worker (See chart “Job openings to unemployed”).

Relative to nominal GDP vs. M2 money supply

Excess savings post 2020 recession

Job openings to unemployed

Today’s conditions are different

In contrast, we now have:

- Money supply growing right at nominal gross domestic product (GDP) growth (roughly 4.5% to 5%) and only 4.9% more M2 relative to nominal gross domestic product (NGDP) than pre-pandemic compared to 28.4% on September 20, 2021 (oh yeah, right when inflation started to become non-transitory). There’s certainly enough available liquidity to drive equity market multiples higher over time given continued reduction in equity supply, but not enough to drive a sustained inflation surge.

- Fed’s reverse repo back close to zero (see chart, “Overnight reverse repurchase agreements: Treasury securities sold by the Federal Reserve in the Temporary Open Market Operations”).

- Excess savings have gone from +$2 trillion to -$800 billion.

- The labor market finally has more unemployed than job openings (99 job openings per 100 unemployed persons). This is the first time this has been the case since the economy was still rebounding from the pandemic in April of 2021.

Overnight reverse repurchase agreements: Treasury securities sold by the Federal Reserve in the Temporary Open Market Operations

Conclusion: Conditions are right for rates to be less restrictive and more neutral

Given that the Fed has spoken about looking through short-term inflation (even Powell), we’ve seen the clear weakening of the labor market, we’ve heard the Jackson Hole comments and seen a substantial slowdown in job creation combined with a modest contractionary fiscal policy coming from tariffs—it is time to bring rates back to a more neutral rate from restrictive.

For investors in floating rate commercial real estate loans or floating rate private credit, this will unfortunately lead to slightly lower income going forward relative to the last 2.5 high base rate years. However, the great news is that in most cases, the income spread to risk free shorter duration investment grade debt and treasuries will expand as it has already done since the Fed cut by 100bps last year. So, if you are focused on income, your future yield pick-up in alternative private credit debt strategies relative to cash should continue to grow over the next few years. Stated another way, “The Time for the Right Alts is Still Now!”