CRE debt: A $6 trillion¹ market opportunity

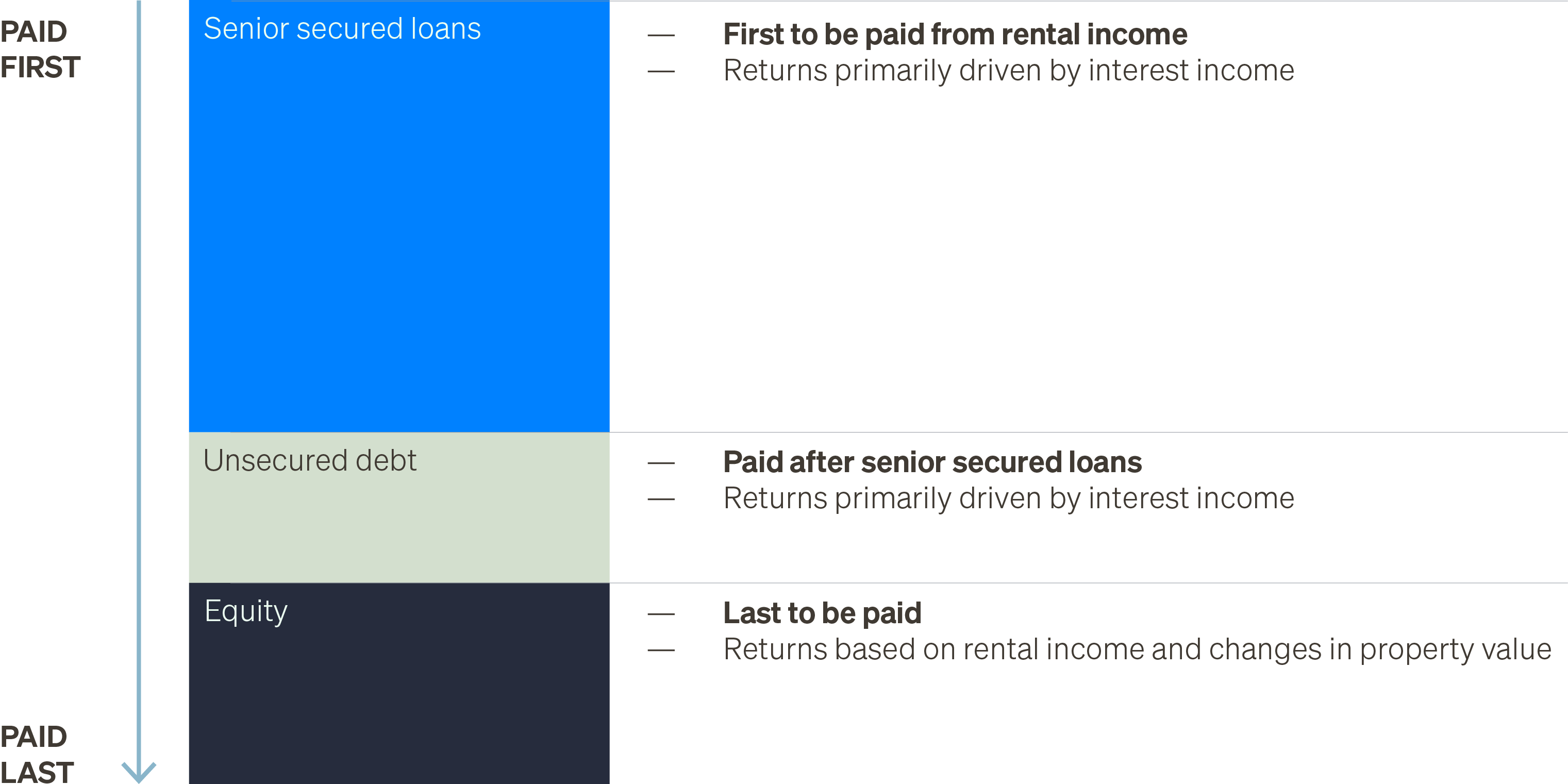

CRE debt: Receiving first priority

Investors in commercial real estate debt serve as lenders to property owners to help purchase, renovate or repurpose a property. An investor’s return is largely driven by the interest income from the loan (or other form of debt). CRE debt investors are paid ahead of property owners, offering greater downside protection if a property’s income declines or value decreases.

Figure 1: Illustrative commercial real estate property capital structure2

A potential source of income and portfolio stability

Commercial real estate debt investors are paid from a property’s income before the property owner, giving them priority in the cash flow of the building. This senior position can help provide more stable income, particularly during periods of market stress or economic downturns.

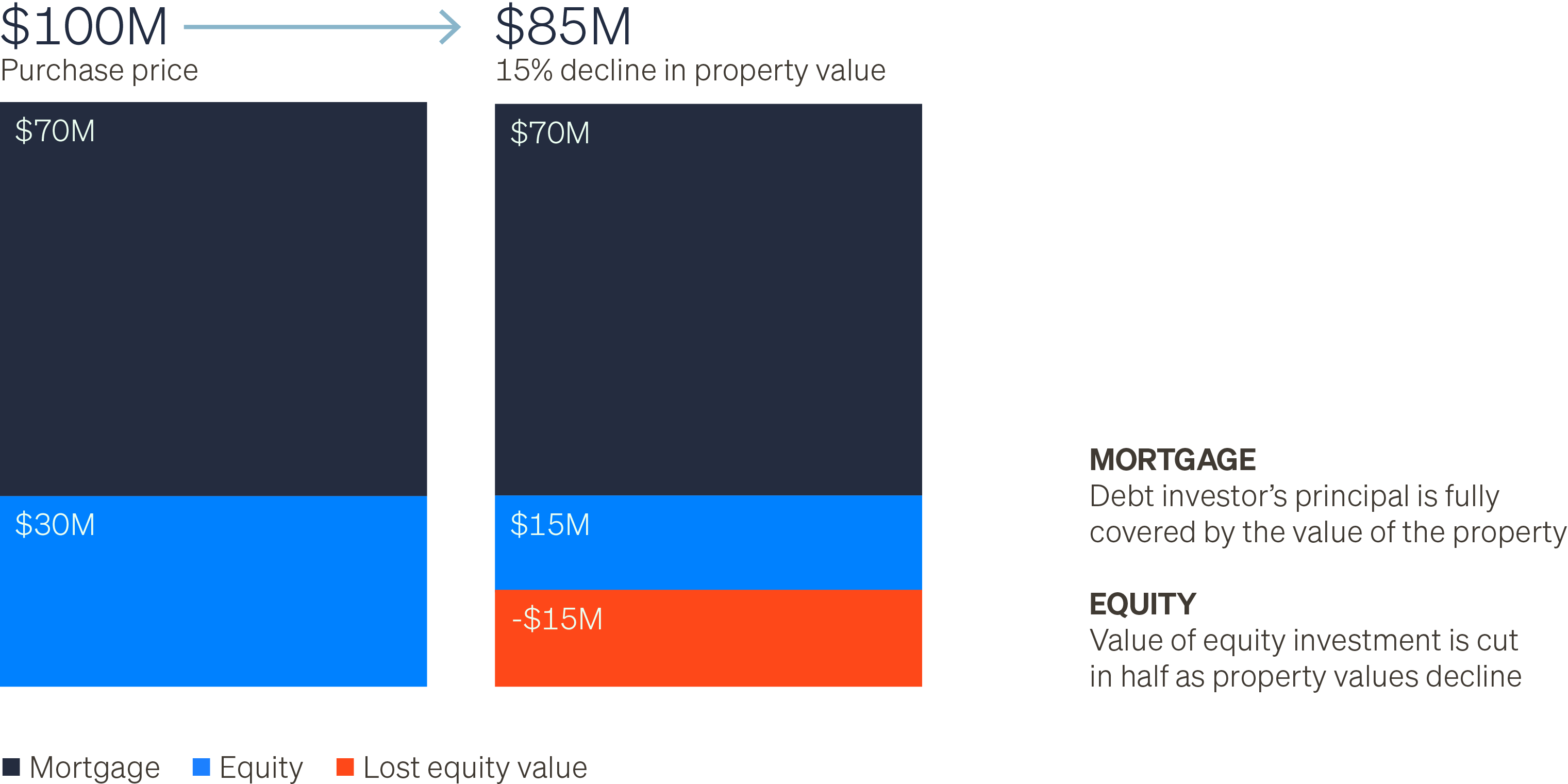

In addition, CRE lenders typically finance only a portion of a property’s value, which creates a cushion against potential losses if property values decline. Using the hypothetical example in Figure 2, if a property’s value falls by 15%, the reduced value still fully covers the mortgage, while the property owner’s equity value is cut in half.

Figure 2: Impact of property value changes, CRE debt vs. Equity investors

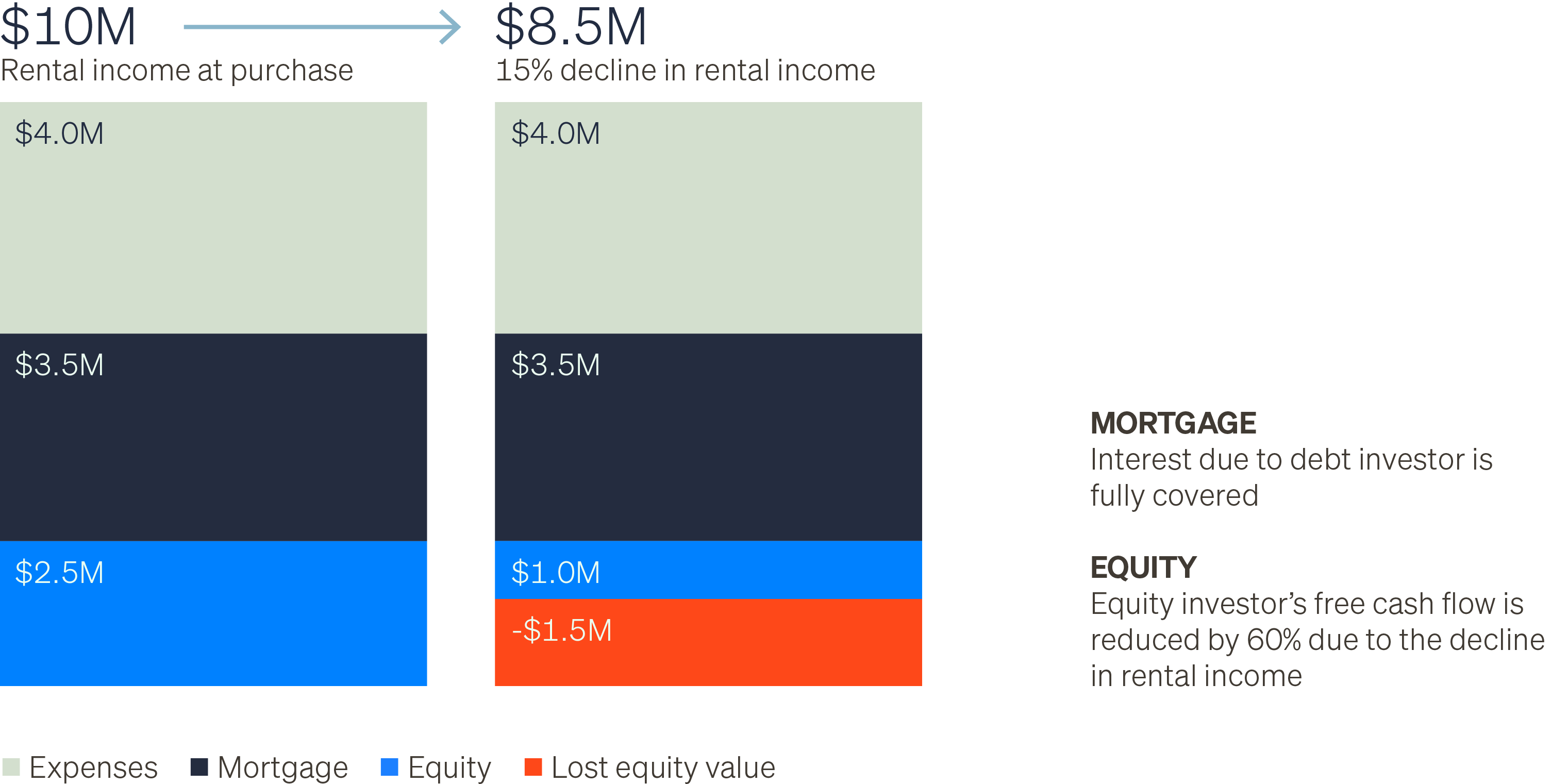

Figure 3 shows how CRE debt investors may also be better protected if a property’s rental income declines, whether from vacancies, renovations or lower market rates. After operating expenses such as taxes, insurance and maintenance are paid, rental income is used next to cover mortgage payments owed to commercial real estate debt investors. Any remaining cash flow goes to the property owner. In this example, the property experiences a 15% decline in rental income. While there is still enough cash flow to cover operating expenses and the mortgage payments, the income flowing to the property owner is significantly reduced.

Figure 3: Impact of changes in rental income, CRE debt vs. Equity investors

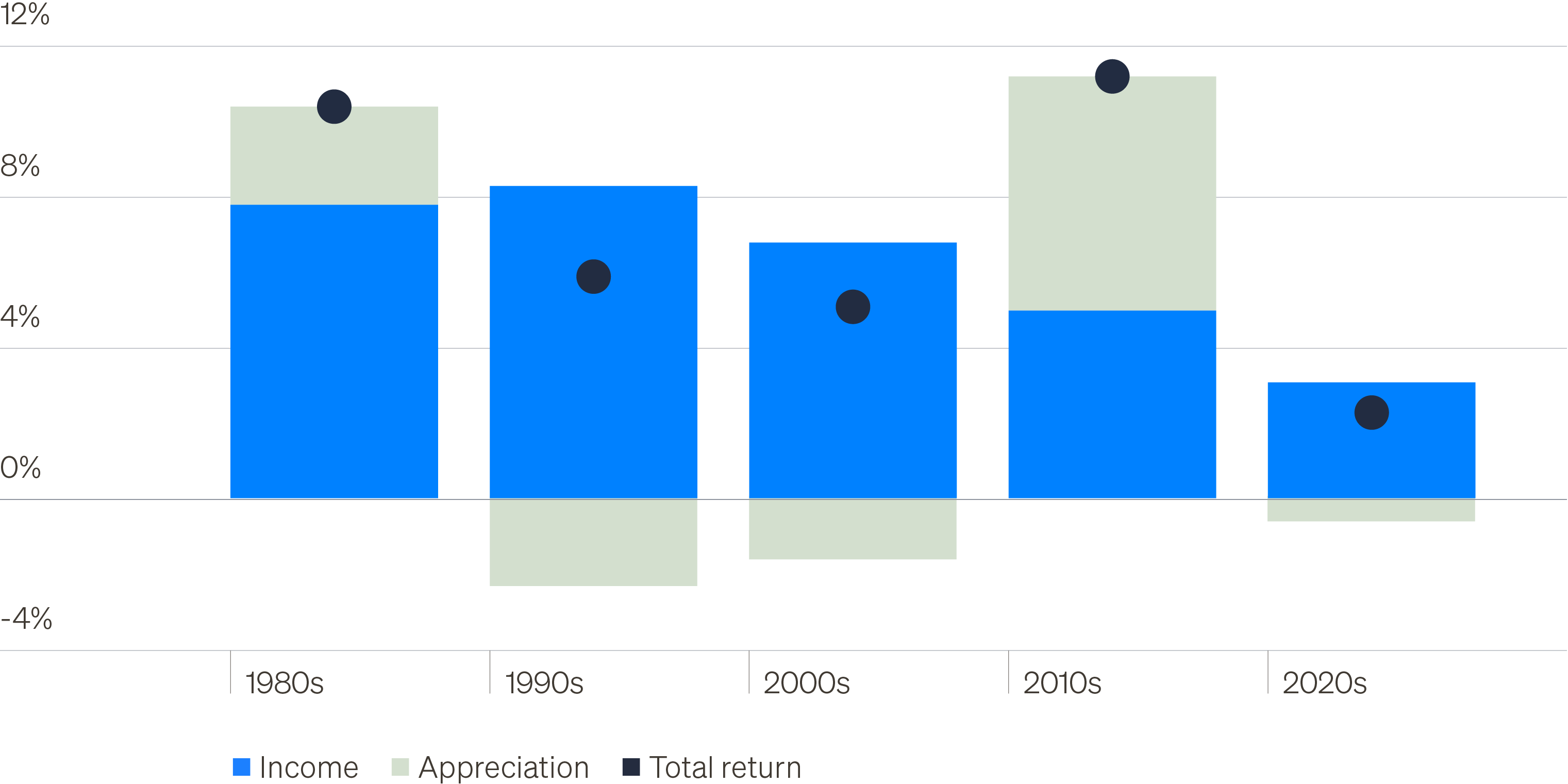

Income is dominant driver of CRE returns once again

Real estate returns have historically been driven by rental income. During the zero interest rate (ZIRP) era of the 2010s, however, falling interest rates lowered borrowing costs and supported cap rate compression, allowing investors to pay higher prices while maintaining target return profiles. As a result, price appreciation became a more significant driver of CRE returns. As rates normalized in 2022 and 2023, higher financing costs and changing return expectations led property values to adjust lower, making income once again the primary driver of CRE returns.

In this environment, investing higher in the capital structure through CRE debt may offer investors an income-focused approach with greater downside than equity ownership.

Figure 4: Commercial real estate returns by decade

Current valuations point to modest future equity returns

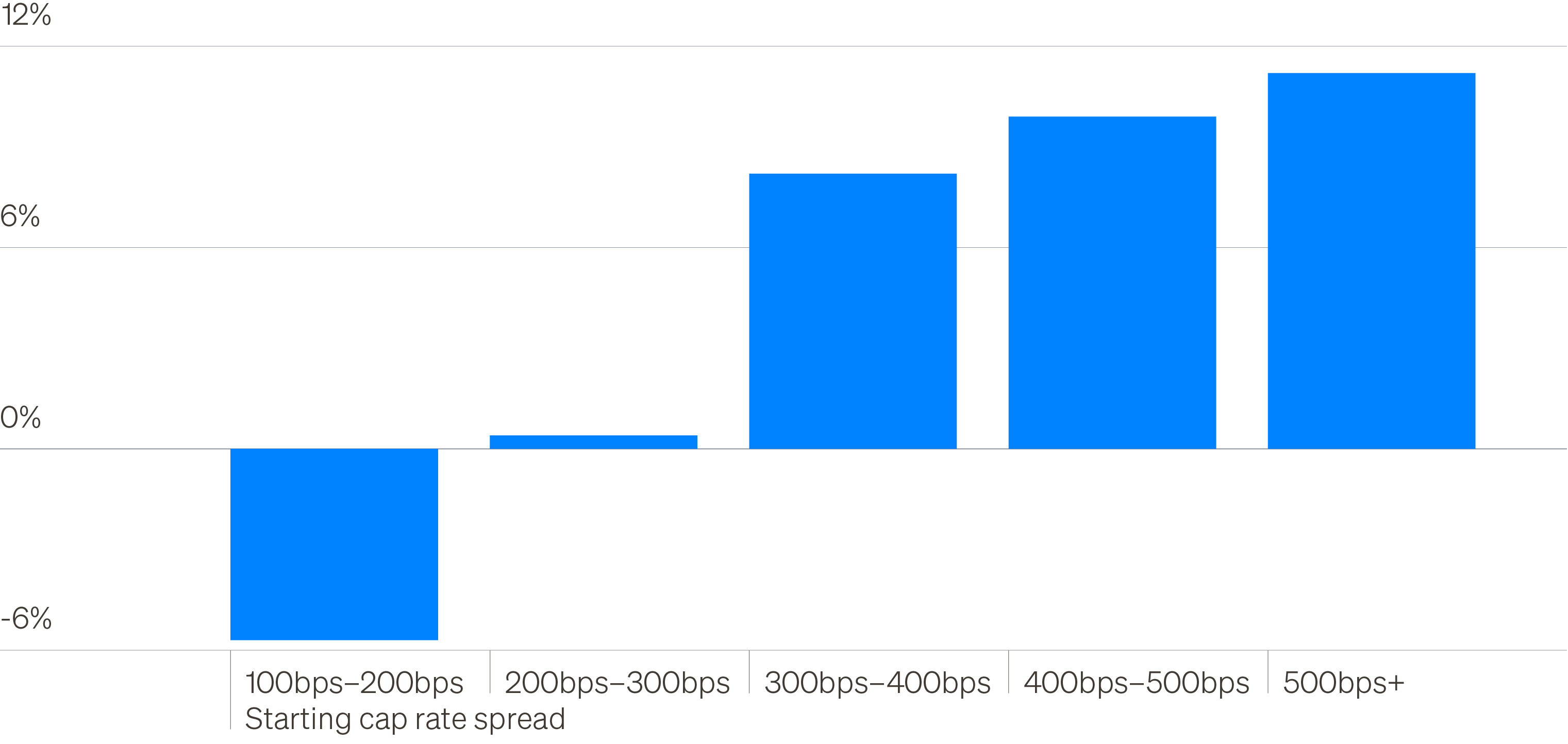

Cap rates are one of the most commonly used metrics to value income-producing real estate. A property’s cap rate is calculated as its net operating income divided by its market price, and it provides a snapshot of the asset’s current income yield. In general, higher cap rates imply higher potential returns, but they can also reflect higher risk or weaker growth expectations.

Because real estate is an income-oriented investment, investors often compare cap rates to U.S. Treasury yields to assess relative value. The difference between the two, known as the “cap rate spread,” is a key indicator of how attractively real estate is priced over time.

When this spread is narrow, forward returns have historically been more limited, with less upside and greater downside risk. For example, when starting cap rate spreads are in the 200–300 basis point range—as they are today—median forward three-year returns have historically been modest (Figure 5).

This valuation backdrop may make CRE debt especially attractive today, offering investors the potential for steady income and greater downside without relying as heavily on property price appreciation to generate returns.

Figure 5: Median forward 3-year returns (annualized)

Investing in CRE debt through real estate investment trusts

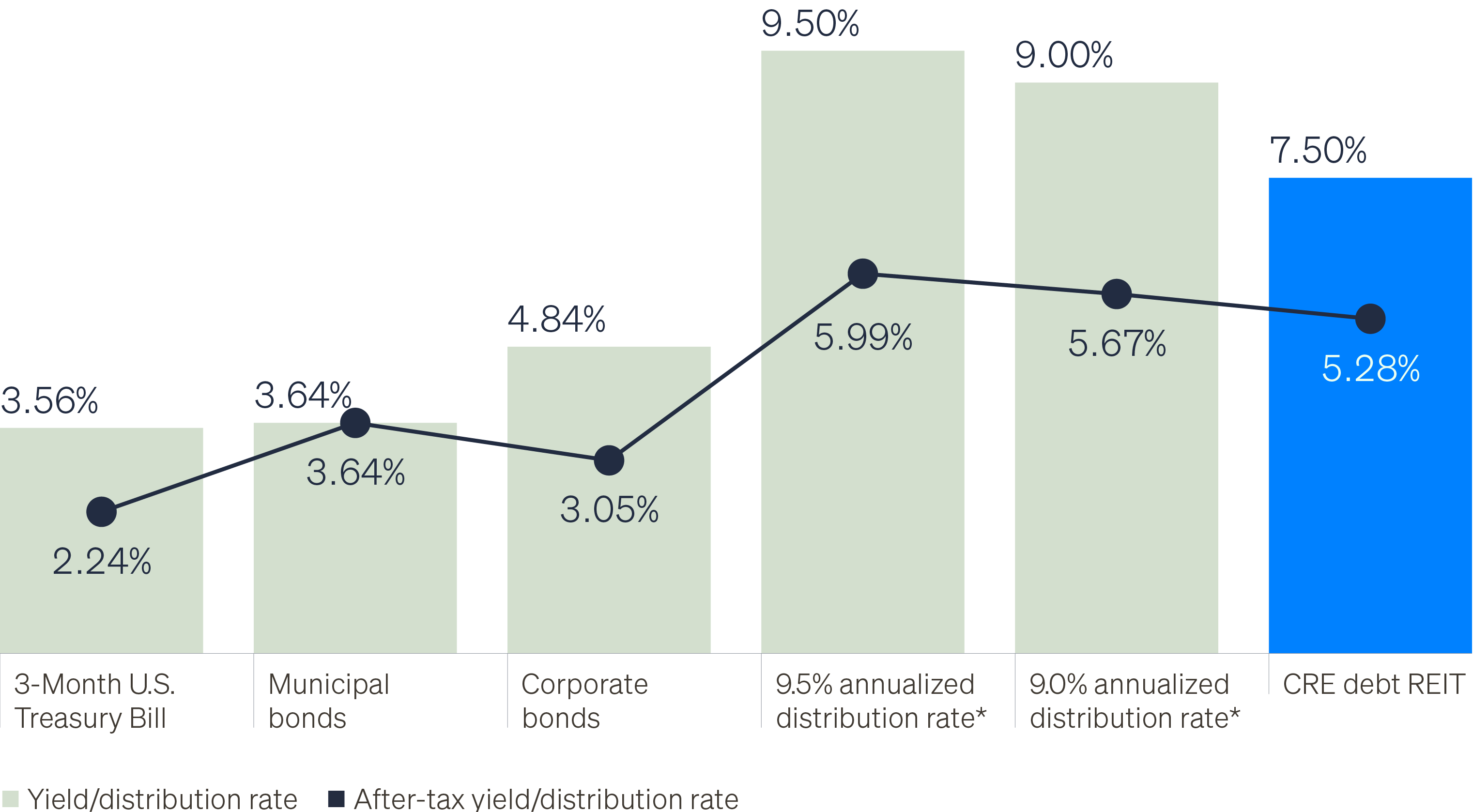

Real Estate Investment Trusts, or REITs, are one of the most common ways investors gain exposure to real estate. They can offer the potential for diversification, income, and a more accessible, lower‑cost alternative to owning properties directly (equity REITs) or lending directly to property owners (debt REITs).

Investors may also benefit from certain tax advantages. Under current tax law, up to 20% of ordinary REIT dividends may qualify for a deduction (excluding capital gain dividends and qualified dividend income), which can lower an investor’s effective tax rate. For example, an investor in the highest tax bracket could see the federal tax rate on ordinary REIT dividends reduced from 37% to 29.6%. This tax benefit is commonly referred to as the Section 199A deduction.

Assuming a REIT pays an annualized distribution rate of 7.5% on a taxable basis, this tax treatment could increase the tax-equivalent rate to approximately 8.4% (Figure 6).

Figure 6: Comparison of REIT distribution rates (assuming 37% tax bracket)*

As illustrated in Figure 7, REITs can offer attractive after‑tax income when compared with many traditional fixed income investments, including higher‑yielding taxable investments.

Figure 7: Current and after-tax yields/distribution rates by asset type4

Summary

Commercial real estate debt may offer investors steady income and greater downside protection by investing higher in the capital structure ahead of property owners. In today’s market, where income has reemerged as the primary driver of real estate returns, CRE debt may provide an attractive source of yield and portfolio stability.