Speed limits

At midyear, the U.S. economy is surrounded by potential inflection points. The war in Iran has paused, at least for now, with oil prices well off their peak. The fiscal impulse from the One Big Beautiful Bill Act (OBBBA) is set to fade. The Federal Reserve is entering a new era under new leadership, just as the policy debate shifts from the timing of rate cuts to potential rate hikes. And businesses are incorporating artificial intelligence (AI) en masse—and in so doing learning about the technology’s capabilities and (significant) costs. But whether these individual turning points add up to an inflection point for the economy itself is a different question entirely.

The defining feature of the U.S. economy since the start of 2025 has been that of offsetting forces. As we discussed in last quarter’s outlook, shocks have become a lasting feature of a new global economic regime defined by fragmentation, competition and technological evolution. The past 18 months have been indicative of that reality. But despite these myriad disruptions and the accompanying uncertainty, the broadest measure of U.S. economic health has remained largely unchanged: Real gross domestic product (GDP) grew by 2.4% in 2024 and, utilizing current estimates for Q2, likely grew by around 2.4% over the past 12 months. This stasis reflects not only the potency of the factors on the positive and negative sides of the ledger, but also the underlying resilience and dynamism of the U.S. economy.1

The push-pull economy: offsetting forces for growth

Estimated impacts on U.S. GDP growth, Today vs. 2024

Note: Current 1-year GDP growth number inclusive of GDPNow estimate for Q2 2026.

It also speaks to the present reality of this cycle: The presence of the AI boom alongside persistently elevated inflation has created economic speed limits—both a maximum and a minimum. When the economic cycle has faced seemingly existential shocks, AI provides a floor via ever-increasing capex budgets and equity prices. When the growth outlook begins to heat up, the presence of above-target inflation creates a quick reaction from the bond market, which acts as a ceiling to depress growth in rate-sensitive industries like housing and autos. These are the speed limits in action. So far this year, better-than-expected growth data has forced a repricing of the Fed path and pushed long-term rates higher, delivering another blow to rate-sensitive sectors. When inflation is elevated, good news is rarely costless.

Rates are enforcing a speed limit

This complex interplay between rates, AI and inflation defines this cycle, but its stability is not a forgone conclusion. Risks rise when growth is concentrated and policy takes center stage—and both of those conditions are present today. Should markets begin to question AI’s profitability path and by extension the capital spending being undertaken, it is not clear there are other growth pillars powerful enough to assume the mantle. Conversely, if the Federal Reserve is seen as uncredible in addressing the inflationary pressures emerging from AI and broader geopolitics, a rapid rise in long-term rates could threaten the expansion. In other words, the AI floor could fall away or the inflation/rates ceiling could cave in.

Our base case for the rest of the year, however, is more “offsetting forces,” keeping growth between 2%–2.5% in the second half.

- On the positive side, an end to hostilities in the Middle East—assuming it lasts—should offer some respite to consumers and take a risk off the Fed’s menu. There does not yet seem to be a credible threat to the AI boom, where capex estimates and earnings continue to surge. And the labor market looks stronger than at the start of the year.

- On the negative side, the Fed’s flip from easing to possibly tightening delivered another blow to rate-sensitive industries, especially housing. The fiscal tailwind from the OBBBA is expected to be cut in half in H2 relative to H1. And the household saving rate has declined to a near-20-year low, calling into question the remaining firepower for consumption.2

For investors, the tails are now more important than the base case. Most portfolios are now dominated by the AI theme, which has also become the largest force for economic growth. Adding more exposure to the theme may come with diminishing marginal benefits while further concentrating risk. Opportunities to source growth outside the AI theme should take priority. Meanwhile, the reemergence of inflation as the key macro variable—and the Fed’s need to address it—has lifted the stock/bond correlation back above +0.5. This further emphasizes the criticality of building truly diversified portfolios while casting doubt on the reliability of duration as an offset to risk.

We will now review our outlook for key segments of the U.S. economy and provide takeaways for growth, policy, rates and portfolios.

Consumers: Powering through

Consumer spending has moderated so far in 2026 amid inflationary challenges, but households remain resilient. The chart below shows real wage growth fell sharply as the war in Iran pushed up energy prices, and consumers responded by dipping further into savings. The decline in the saving rate from 4.9% to 3.0% over the past year is responsible for funding nearly all of the 2.1% real growth in consumer spending2, and consumers have undoubtedly been steeled by surging equity values: Even households outside the richest decile have seen the value of their equity holdings rise by nearly $3 trillion in aggregate over the past two-and-a-half years. With interest rates and inflation having risen and forced the saving rate near a 20-year low, it is reasonable to question how much firepower is left in the wealth effect.3

Despite these stressors, the macro picture remains broadly healthy. Leverage is low and many households are sitting on significant untapped wealth in their homes and brokerage accounts. Wage growth has cooled somewhat, but its moderation is overstated: Outside of a (strange) slowdown in health care, overall wage growth continues to run close to 4% per annum.4 A potential lasting end to hostilities in the Middle East would provide meaningful relief, especially for lower-income households most exposed to energy prices. Consumers powered through the energy shock, relying on a combination of savings and higher tax refunds. Those sources of dry powder are less potent now, but fundamentals continue to support solid, steady consumption growth.

Consumers are strained but resilient

Sources of annualized real spending growth, by half year

AI business investment: Reaching new heights

The investment categories relevant to the AI infrastructure buildout (data centers, technology equipment and software) now comprise 40% of nonresidential private investment, up from 20% a decade ago.2 Similarly, the five major AI hyperscalers now account for one-third of all S&P 500 capital expenditures. Analysts have consistently underestimated the scale of AI-related spending, with forecasts for full-year 2027 now surging toward the $1 trillion mark, up from $600 billion just six months ago. While some of this reflects the rising cost of data center components—an increasingly important trend for inflation—most of it reflects an explosion in demand for compute.5

The agentic tools enterprises are implementing for complex workflows use an immense quantity of tokens and, by extension, compute. As corporate implementation became tangible in the first half of this year, the major questions facing the AI buildout shifted—from whether demand would materialize to supply bottlenecks, rising costs for AI users and public backlash around data centers. AI capex has become a meaningful segment of the U.S. economy growing at an incredible pace. That growth comes with clear downside risks, but it is more likely than not that spending budgets will go up—not down—over the balance of the year.

Consensus estimate for annual AI hyperscaler capex

Note: AI hyperscalers include Amazon, Alphabet, Microsoft, Meta, and Oracle.

Non-AI business investment: Green shoots

Companies outside the immediate AI ecosystem have not participated in the recent capital spending boom—in fact, real business fixed investment excluding AI-relevant items has detracted from GDP growth in recent quarters. To some extent, AI-powered growth has capped non-AI business investment by keeping interest rates elevated and siphoning resources. However, there were encouraging signs of broadening in the first half. Earnings growth has accelerated across the market which—along with attractive tax incentives offered by the OBBBA—may be giving firms the green light to invest.

Some of this broadening likely reflects AI impacts permeating other sectors. Utilities, energy and industrial companies may not technically be direct AI plays, but many of them are experiencing a boost in demand from the data center buildout that is catalyzing investment. And while elevated rates are a genuine headwind, debt financing remains available and reasonably priced. We expect secular themes like AI and defense to remain the dominant drivers of capex growth. But as those themes spread through the economy and earnings growth broadens, the environment for business spending should improve.

ISM signals broadening of capex theme

Note: ISM represents three-month moving average.

Note: Capex numbers exclude the tech sector, Amazon, and interactive media industry, as well as the financials and real estate sectors.

Housing: Unable to gain traction

The housing market continues to suffer the consequences of resilience in the rest of the economy. Put simply, at today’s home prices and mortgage rates, there are not enough buyers to support a recovery. Affordability has improved on the margins, but the recent uptick in mortgage rates following the start of the war in Iran ensured a fourth consecutive soft spring selling season. Builders, who are sitting on more than nine months of supply, remain cautious in breaking ground on new projects.

The housing market remains in the same straitjacket it has worn since the Fed raised rates. Affordability must improve to boost demand; absent a decline in rates, prices must fall to improve affordability. The surest way for prices to fall is rising for-sale inventory—but with half of homeowners still holding a mortgage rate of 4% or lower, the cost of selling is significant.6 Lower rates would, in theory, boost both demand and supply—a positive outcome for the market as a whole. But with inflation elevated and the labor market showing signs of strengthening, that “quick fix” appears unlikely. The best thing we can say about the housing market is it is not worsening materially. Activity is sluggish, price growth is geographically varied but near flat overall, and rates remain the most important input for the outlook.

Number of home sellers per buyer

By U.S. census region

Labor market: Incremental improvement

Labor market data improved over the first half of the year, largely stemming concerns around broader weakness that were present at the start of 2026. The most significant shift has been the uptick in hiring—the economy added an average of 114,000 jobs per month through May, compared to modest job losses over the second half of 2025. We are skeptical this level of hiring is sustainable—estimates for the breakeven hiring rate sit around 20,000–40,000 per month, and business surveys do not indicate a pickup in hiring intentions. Even still, the economy is creating enough jobs to have kept the unemployment rate flat over the past year at a low level of 4.3%—ultimately the most important signal.4

There is scant evidence of any large-scale impact of AI on the labor market to date, despite some high-profile layoff announcements and growing worker anxieties. To the extent firms are supplanting human labor with the artificial variety, it is most impactful for new labor market entrants (especially recent graduates) rather than existing employees. We see the jobs backdrop today as stable and bordering on strong. Solid wage growth and elevated participation reflect a labor market that, while less dynamic than a couple years ago, continues to support healthy economic growth.

Hiring diverges from underlying sentiment

Note: Both series show three-month moving averages.

Inflation: A rotten core

Inflation worsened during the first half of 2026, due partially—though not entirely—to disruptions related to the war in Iran. Energy prices should continue to fall from peaks if the ceasefire proves durable, though are unlikely to return quickly to pre-war levels. More salient for policymakers is excess core inflation, which can be traced to three broad factors: Continued healthy wage growth, AI data center impacts and tariffs. Disentangling the structural from the ephemeral effects is challenging, which is why we focus on the aggregate: Core PCE has risen by 3.4% over the past year and by 4.2% annualized through the first five months of the year.2

AI-driven productivity gains may eventually prove disinflationary, but today its economic impact is dominated by the large-scale infrastructure buildout, which is increasingly becoming inflationary. Supply shortages are driving up the prices for gas turbines, memory chips and other components and machinery. Direct impacts on consumer prices are minimal thus far, but rising input costs run the risk of being passed on. The inflation backdrop has not improved in two years, and arguably worsened in the first half of 2026, even excluding the Iran War. Improving labor market data and emergent pressures from the AI capex boom are likely to keep inflation elevated through the end of the year.

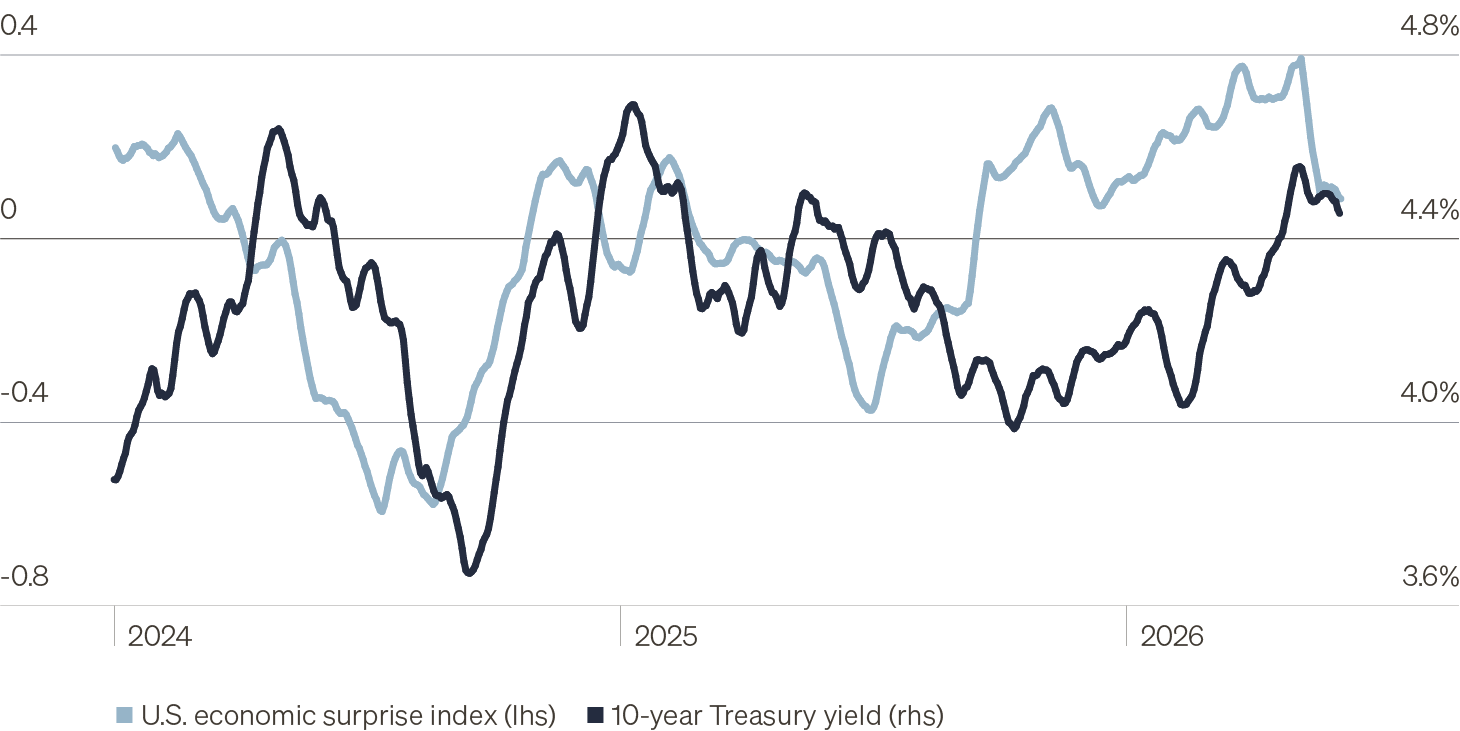

Markets remain sanguine despite inflation turn

What does this all come to? Investing within the speed limit

The most likely outcome is not a clean acceleration or a clear downturn, but a continuation of the uneven resilience that has persisted for much of the past two years. AI-related investment remains powerful enough to support growth, while persistent inflation and higher rates remain restrictive enough to limit how broadly that growth can spread. Consumers and labor markets are still solid. There are no clear signs the U.S. economy is either breaking or broadening significantly.

There is, of course, a path that provides a positive escape hatch from the speed limit regime: A durable rise in productivity growth. There is enough evidence to suggest productivity growth in the U.S. has risen compared to pre-COVID, and AI provides an impetus for further improvement. While we are optimistic such a scenario will eventually materialize, today the improvement is relatively modest and centered mostly within the technology industry.

This leaves us with three macro conclusions for the second half:

For investors, it is important to remember that a benign macro base case is already priced, and thus it makes sense to focus on ensuring portfolios are built for the tail risks. We are focused on three priorities:

- Search out non-AI sources of growth. AI remains the economy’s most important marginal growth engine, but it is also embedded across portfolios through hyperscalers, semiconductor companies, infrastructure suppliers and—after the upcoming slate of mega IPOs—model developers. Our view is not that AI exposure should be avoided; it is that simply adding more of it may increase concentration risk faster than it offers marginal benefits. A premium should be placed on companies and strategies that can generate growth from less crowded channels, and those who can benefit from the utilization of AI, not just its creation.

- Take advantage of higher rates, but don’t bank on them falling. We seem to be at an inflection point for Fed communication, as new Chair Kevin Warsh looks to wean markets off their obsession with every syllable coming out of a Federal Open Market Committee (FOMC) member’s mouth. That said, there are few signs he will have the ability, or even interest, to push for lower rates. The Fed is on hold today, and rate hikes in the second half of the year appear increasingly possible. Floating-rate credit offers a compelling risk/reward in this environment, while duration looks less reliable as both a return source and a portfolio hedge.

- Diversification is more than a buzzword. Many investors do not prioritize diversification until it is too late, but markets are providing an opportunity for preemption today. The stock/bond correlation has moved firmly into positive territory again amid higher inflation and a Fed pivot. Meanwhile, concentration in equity portfolios has reached near-record levels. It has never been more important to build a portfolio that is truly diversified—not simply by traditional asset class, but by economic exposure.