Questions surrounding the growth of private credit are both inevitable and warranted. The asset class has expanded rapidly, garnering attention at nearly the same pace that it has taken share within credit markets. Yet in many cases, the scrutiny has come in the form of anecdote and narrative rather than objective analysis. A market that now comprises thousands of loans and nearly $1.5 trillion in U.S. assets will inevitably experience its share of defaults and losses. But do those instances signal systemic weakness? For investors drawn to private credit’s resilient yield premium over public markets, this is the central question.

We find the current private credit discourse heavy on headlines and flimsy on framework. Claims of overheating or fragility are rarely tested against consistent historical criteria that have defined true financial bubbles in the past. This paper seeks to fill that gap. Part 1 establishes a clear definition and analytical framework for identifying when a market has entered bubble territory. Part 2 applies that framework to private credit today, addressing the most common questions we receive about its underlying health, risk dynamics and linkages to the broader financial system.

Our findings suggest that while vigilance is always warranted in credit markets, none of the defining markers of a bubble are present today. Investors will need to be more selective as the market grows and expands, but concerns around the fundamental stability of private credit appear to us unfounded.

Part 1: Our credit bubble framework

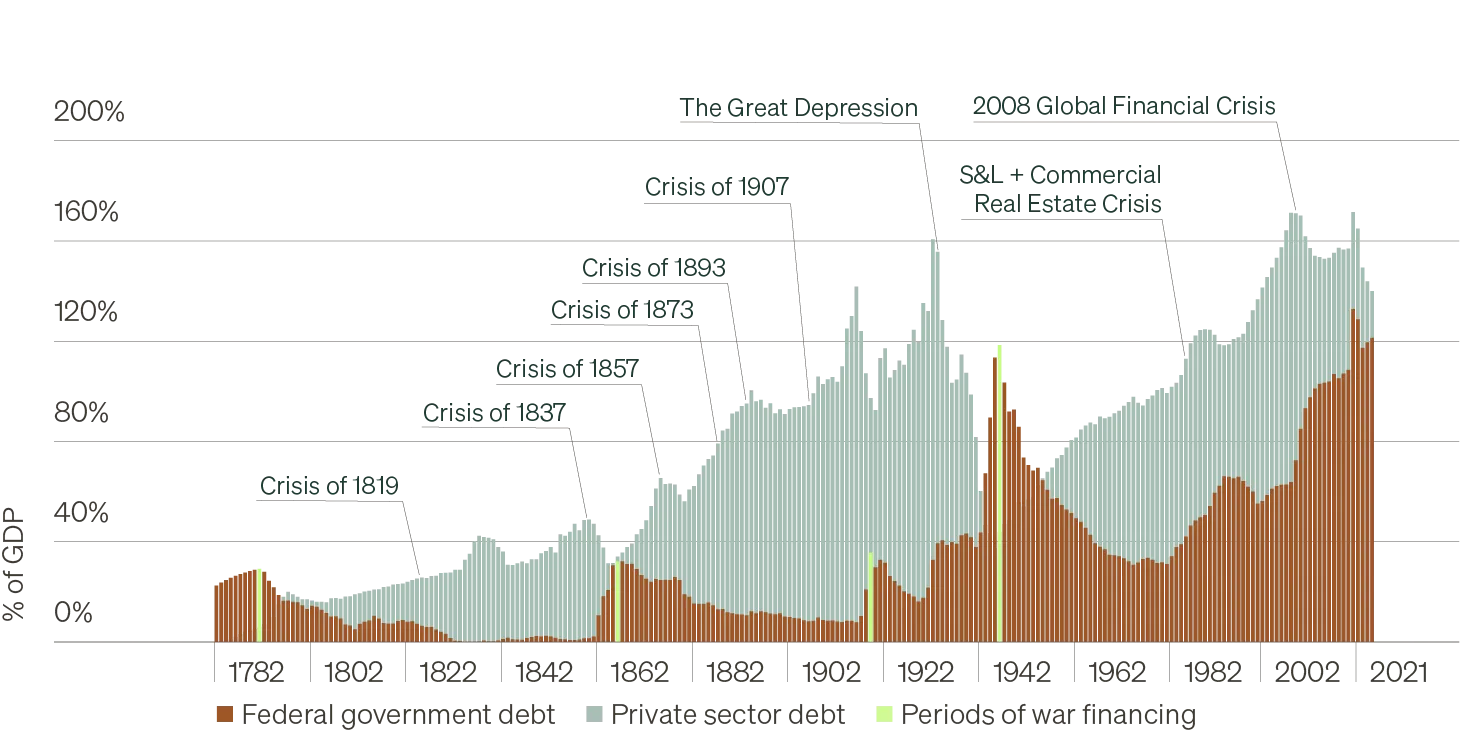

A credit bubble forms when loan growth far outpaces true economic demand, inflating asset valuations, encouraging still more lending, and ultimately creating overcapacity and debt that incomes cannot support. As defaults rise—often amplified by hidden leverage—losses erode lender equity, confidence breaks down, and asset prices undergo a painful, prolonged correction. As the charts below show, neither aggregate private-sector debt nor leveraged credit exhibit these classic warning signs. The conclusion of our framework is clear: private credit’s expansion reflects a larger share of the debt pie, not an enlargement of it.

U.S. debt, financial crises and wars (1782—2021)

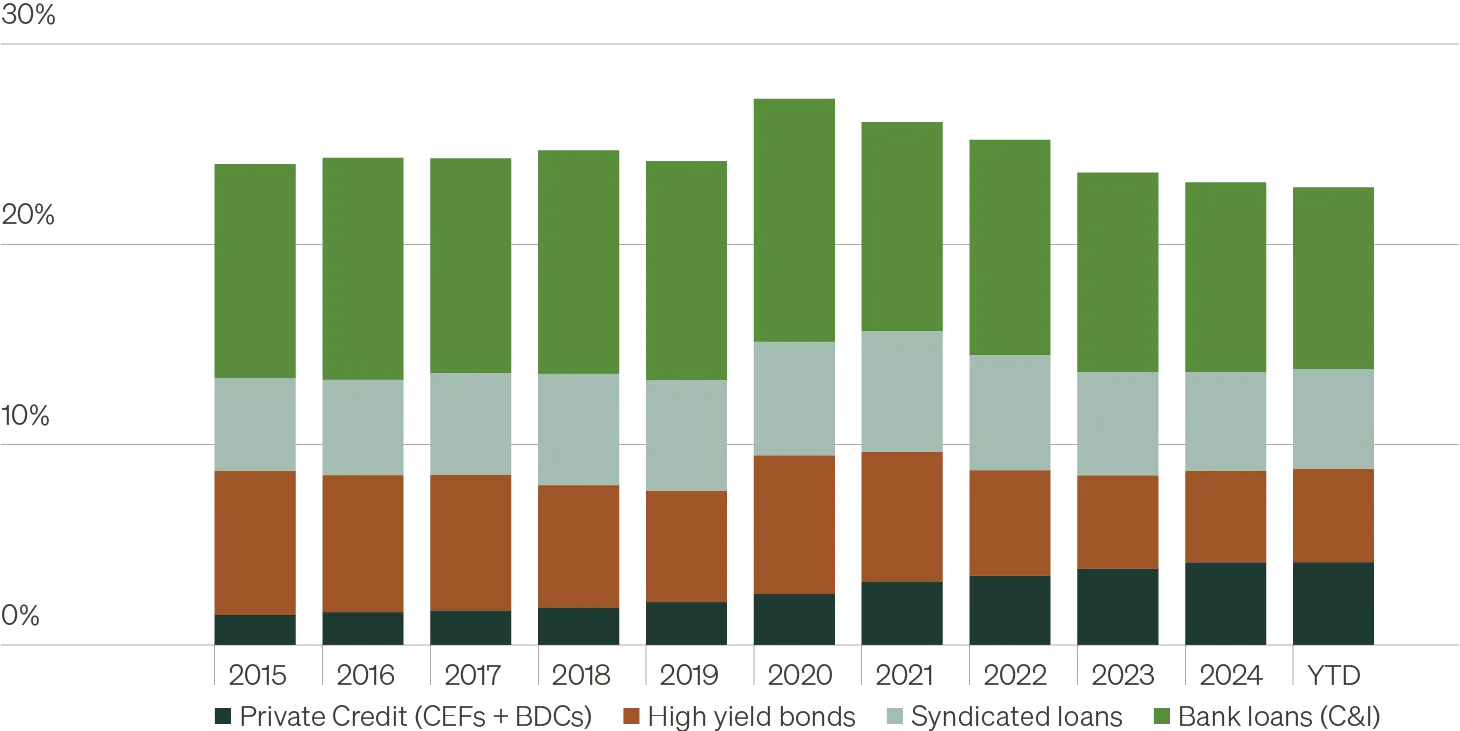

Leveraged credit as a share of nominal U.S. GDP (%)

Part 2: Private credit health check-in

Private credit’s rapid expansion has naturally raised questions about the market’s durability. The inquiries we receive most often center on three areas: whether fundraising is aligned with deployable opportunities; the health and direction of underlying loan fundamentals; and the implications of deeper linkages between private credit managers and banks. The executive summary below distills our core views across these themes, while the full report provides a comprehensive analysis.

Conclusion: A bubble does not lead a quiet existence

Ultimately, we believe concerns as to whether private credit is a bubble most often arise from an imperfect definition of the term, combined with the improper extrapolation of anecdotes. History instructs us to keep things simple: Without excess credit growth, there cannot be a credit bubble.

This is not to say the market has not changed as it has grown. A sterling history of excess returns versus public credit markets has attracted new entrants and fresh capital. When deal activity has been slow, those lenders rapidly fundraising have almost certainly felt greater pressure to win deals, and win bigger deals, to get capital deployed. Although this may reflect a market that could be described as “hot,” it may also reflect a market simply maturing into a more competitive state. One where the era of easy is over and specialization and diversification are now requisite.

After all, assessing whether a market is hot is an observation made relative to the starting point. Skilled first movers in private credit capitalized on the combination of a highly fractured and inefficient market supported by an emerging long-term megatrend that has reshaped the provision of credit. That the market is now more competitive is to be expected but still relative. The baseline is important—room temperature is substantially hotter than ice cold, but is it hot? It depends on perspective. But what we can be certain of is the question of whether a bubble exists isn’t relative, it’s absolute. Is the water scalding hot? If I put my hand in it, am I certain to be burned? That’s a bubble.

We understand investors’ concerns about private credit’s rapid growth, but that growth has been decades in the making. As regulators have strengthened the banking system, banks have consolidated, retreated from certain business lines, and prioritized capital efficiency. Simultaneously, investors across the spectrum have sought to optimize income generation and diversification in their portfolios. Private credit sits at the intersection of these forces. Like all lending markets, it will experience periods of stress and defaults, but there is little to indicate that recent anecdotes reflect anything systemic.

We hope this report has provided an objective lens through which to analyze the health of private credit, one that goes beyond headline-surfing. Our analysis demonstrates none of the signals of a credit bubble are present, private credit borrowers remain generally healthy and the asset class continues to offer investors a substantial yield premium over investments with similar risk profile.