The U.S. economy enters the fourth quarter riding an uneasy momentum. Growth is resilient, inflation is simmering and the labor market has weakened. This distinctive combination of factors has created a benign backdrop for markets, as consumer spending and artificial intelligence (AI) investment has kept earnings growing apace, while the labor market has softened enough to elicit rate cuts from the Fed—but not so much that it yet threatens the business cycle.

For the next quarter, we expect a continuation of the curious “strong but uneven” theme that has persisted for the past five months.

Go in-depth on the forces shaping the U.S. economy in Q4, what’s next for asset classes across public and private markets and what these trends mean for investors.

Macro house view

- Economic growth: Economic growth has outpaced the consensus since the end of Q1, as forecasters underestimated the resilience of consumers and the potency of the AI capex boom. After a strong Q3, 2% seems a reasonable baseline for overall real growth in the short term.

- Labor market: The labor market is challenging to pin down at present. Hiring has plunged, but at least part of that is attributable to immigration policy, while AI is likely also playing a role. Layoffs remain rare and employment levels are strong, but dynamism is gone and households are concerned about job-finding prospects. We expect resilience to continue in Q4 but downside risks are clearly present, warranting Fed attention.

- Consumers: Consumer spending has reaccelerated and grown at a 2.5% annualized pace since the end of March. A portion of this strength can be attributed to a falling savings rate compensating for slow income growth. Still, households are in healthy shape and it is reasonable to expect consumers will continue to power growth.

- Businesses: AI-related investment is surging and has become the most important macro theme, while most other types of business investment are stagnant or sliding. Lower rates are already spurring M&A and debt issuance activity, a positive sign for business confidence.

- Housing: Home price growth is wavering as existing home inventories have finally increased, especially in Sun Belt and Mountain region markets. Prices are falling gradually in these markets, and residential investment remains a detractor from growth. Lower short-term rates are likely to lift housing activity only on the margins.

- Inflation: Tariffs’ impact on inflation has been noticeable but limited. Core inflation is running one percentage point higher than the Fed’s target, with little progress since the end of 2023. Tariff effects will likely become more noticeable in Q4.

- Monetary policy and interest rates: The Fed has eased and will cut at least once more in Q4. The outlook beyond that is dependent upon stabilization in labor market data. History tells us that without a recession, long-term rates usually rise after the Fed’s initial rate cut.

The categories of business investment where most AI infrastructure investment is captured—largely data centers, the hardware that goes inside data centers, and software—have added 0.8 percentage points to GDP growth over the past year.

Contribution to U.S. trailing one-year real GDP growth

Asset class views

- U.S. equities: The S&P 500 is set for a third consecutive year of stellar performance. AI-related stocks, which now make up more than half the index, have driven the bulk of the gains. The U.S. tech sector is dynamic, but record concentration and valuations warrant a focus on identifying diversifying exposures.

- Core fixed income: Bonds have had a strong year as long-term rates have declined in anticipation of Fed cuts, but significant further declines are likely only in the case of recession. Bonds’ correlation with stocks has remained in positive territory this year.

- Cash: The Fed is easing and inflation remains elevated. Real short-term yields could be around 0% by the end of next year, limiting the portfolio case for cash holdings.

- Private equity: Deal activity has been sluggish for two-and-a-half years but is showing signs of life amid economic resilience and lower rates. PE’s next era will be defined by operational value creation, not leverage and multiple expansion. Valuations, leverage and foreign dependency are all lower in the middle market, making it favored over mega-cap funds.

- Private credit: Spreads across credit have tightened and short-term rates are coming down, but underwritten returns in private credit remain compelling. We favor a diversified approach, pairing large-cap direct lending with more specialized, less competitive segments like lower middle market direct lending and asset-based finance.

- Commercial real estate: Sentiment has ebbed and flowed throughout the year, but the market appears on course for a gradual rebound. Lower short-term rates should feed a recovery in deal volume, but property values are likely rangebound for the foreseeable future.

Implications for investors

What do our macro views mean for investors and allocators?

- Equities: The U.S. remains the most dynamic investable market in the world, but investors are highly exposed to AI risk via both the market and the economy. Private equity—particularly strategies focused on the middle market—can diversify a large-cap equity allocation while also offering growth and a reasonable valuation entry point.

- Fixed income/credit: Bonds benefited from falling long-term rates ahead of Fed cuts, but that trend has likely run its course unless a recession materializes. Better covenants and pricing favor private credit over public credit, but investors should seek out less competitive segments to maximize yield per unit of risk.

- Real assets: Elevated inflation, surging capital spending, falling construction activity and a housing shortage create a compelling case for real assets. We favor segments that will thrive in an income-dominated return backdrop, including real assets debt and core-plus strategies.

Executive summary

Given the potentially profound impacts from AI implementation, as well as tariff and immigration policy that reflect sharp departures from recent decades, today’s economic backdrop is a particularly challenging one around which to wrap a cohesive narrative. Are we in the early stages of a productivity boom, or is AI investment masking an otherwise frail economy? More clarity will likely emerge in the new year; for Q4, we expect a continuation of the curious “strong but uneven” theme that has persisted for the past five months.

The incredible equity gains created by the AI boom have boosted the wealth of U.S. households to heretofore unseen levels.

Ratio of household wealth to annual spending by household income quintile

Read the complete executive summary for key insights into how AI represents a macro “swing” factor, what labor market stagnation means for investors and where market uncertainty represents both negatives and positives.

Themes in focus

Explore key themes driving markets in Q4:

Sentiment segmentation: Who is right?

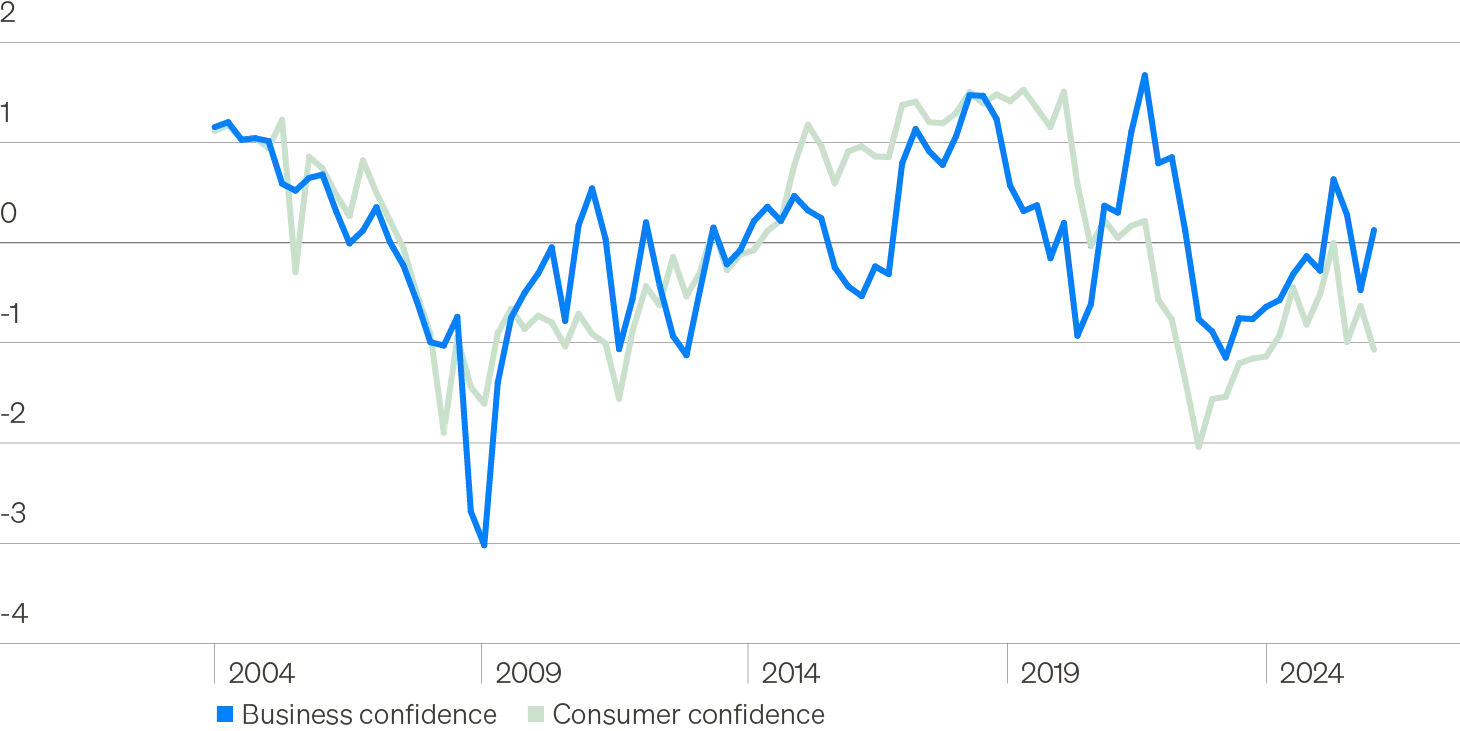

One trend we have been following for some time is the persistent gap between soft economic indicators—such as surveys—and hard indicators like consumer spending and GDP growth. This gap has narrowed in certain areas, most notably the labor market, but hard data has broadly outpaced soft data consistently since 2022. This has resulted in an understandable reexamination of the usefulness of surveys, particularly as a means of predicting future economic activity. Over the past few months, a new gap has opened up within sentiment indicators, as consumers, businesses and investors are all feeling differently about the current economic environment.

Business vs. consumer confidence

Note: Business confidence is a combination of the Duke CFO Survey, Conference Board CEO Survey, Business Roundtable CEO Survey, and NFIB Small Business Survey. Confidence metrics shown are average z-scores for component indexes using data back to 2004.

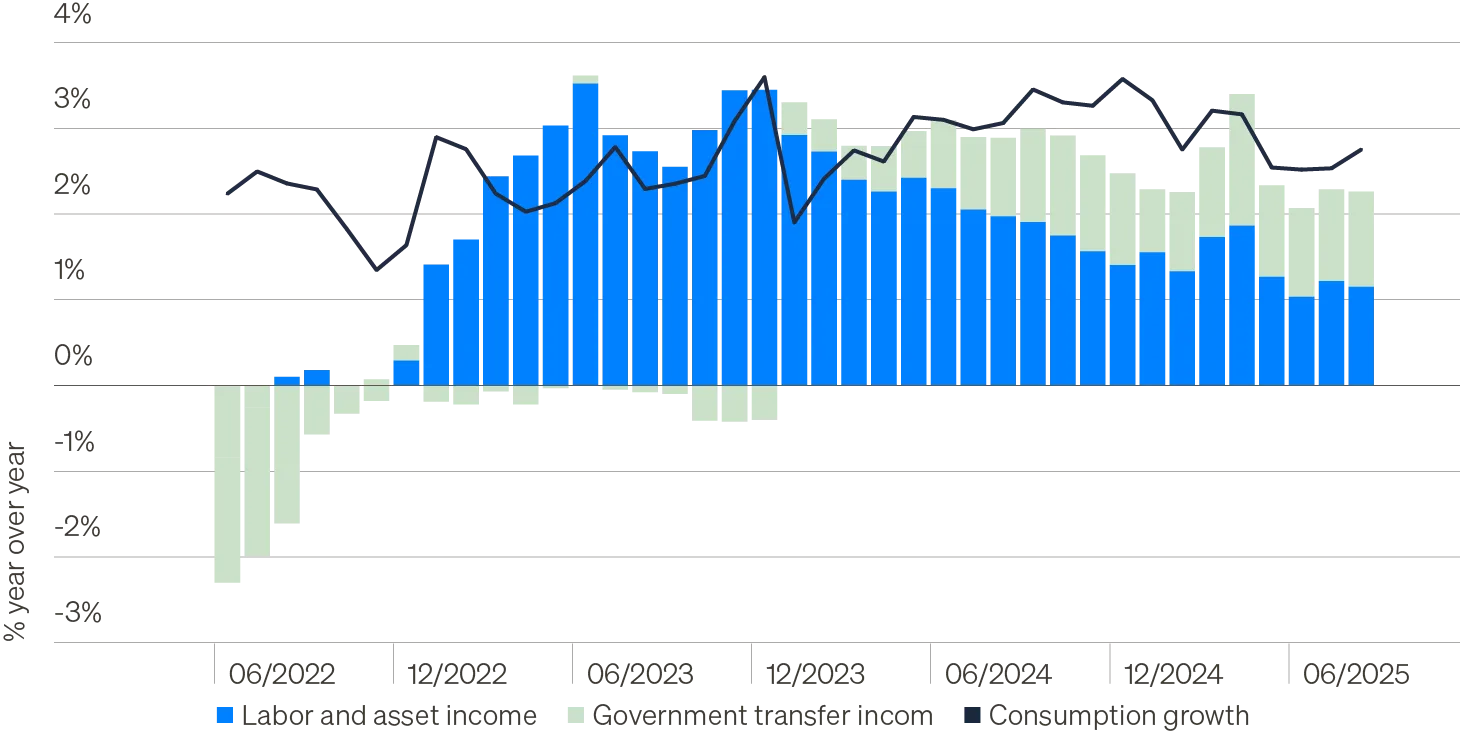

Spending and income: How long can they diverge?

Since the tariff shock of Q1, U.S. consumers have generally continued to spend at the pace they had been in 2023 and 2024. Real consumption has risen at a 2.5% annualized pace since April, a level consistent with a healthy economy.1 However, this strength stands in contrast to slowing real income growth, which is the chief funder of household consumption. With population growth stalled by immigration policy and wage growth at risk of moderating, it is reasonable to expect that aggregate household income growth will remain challenged. The question is whether that presages a slowdown in consumer spending.

Components of real personal income growth

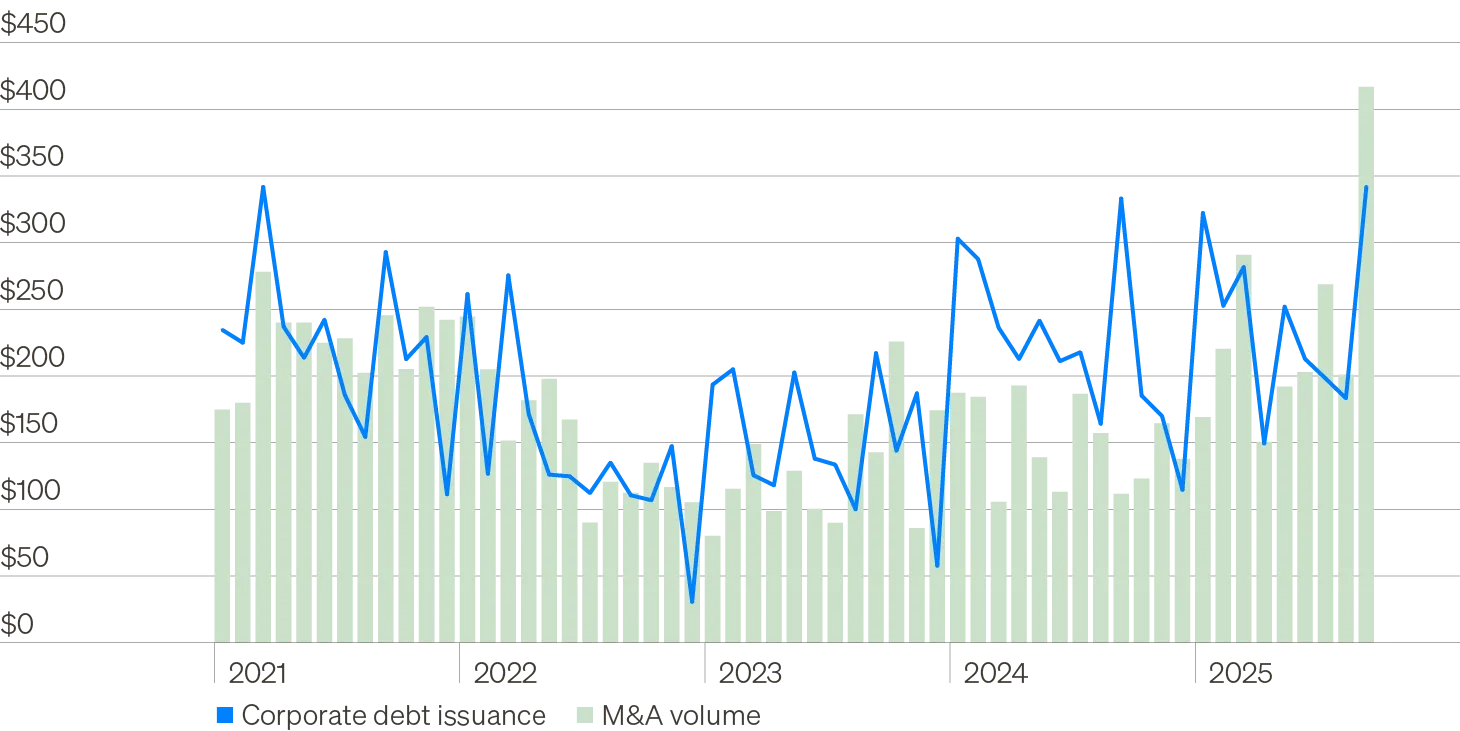

Where to look for rate cut impacts

The Federal Reserve reduced its policy rate by 100bps over the final four months of 2024, paused for nine months and then in September returned to easing by cutting another 25bps. Markets currently expect two additional rate cuts in Q4, and between two and three more in 2026, bringing the Fed funds rate to 3% by the end of next year. We see material risk the Fed does not meet these lofty easing expectations.2 Labor markets have softened in recent months but equity markets are near all-time highs, GDP growth is solid and inflation remains above target.

U.S. monthly corporate M&A and issuance activity ($ billions)

Note: debt issuance is comprised of gross issuance activity for investment-grade bonds, high yield bonds, syndicated loans, and direct lending deals. M&A volume includes corporate M&A and private equity investments.

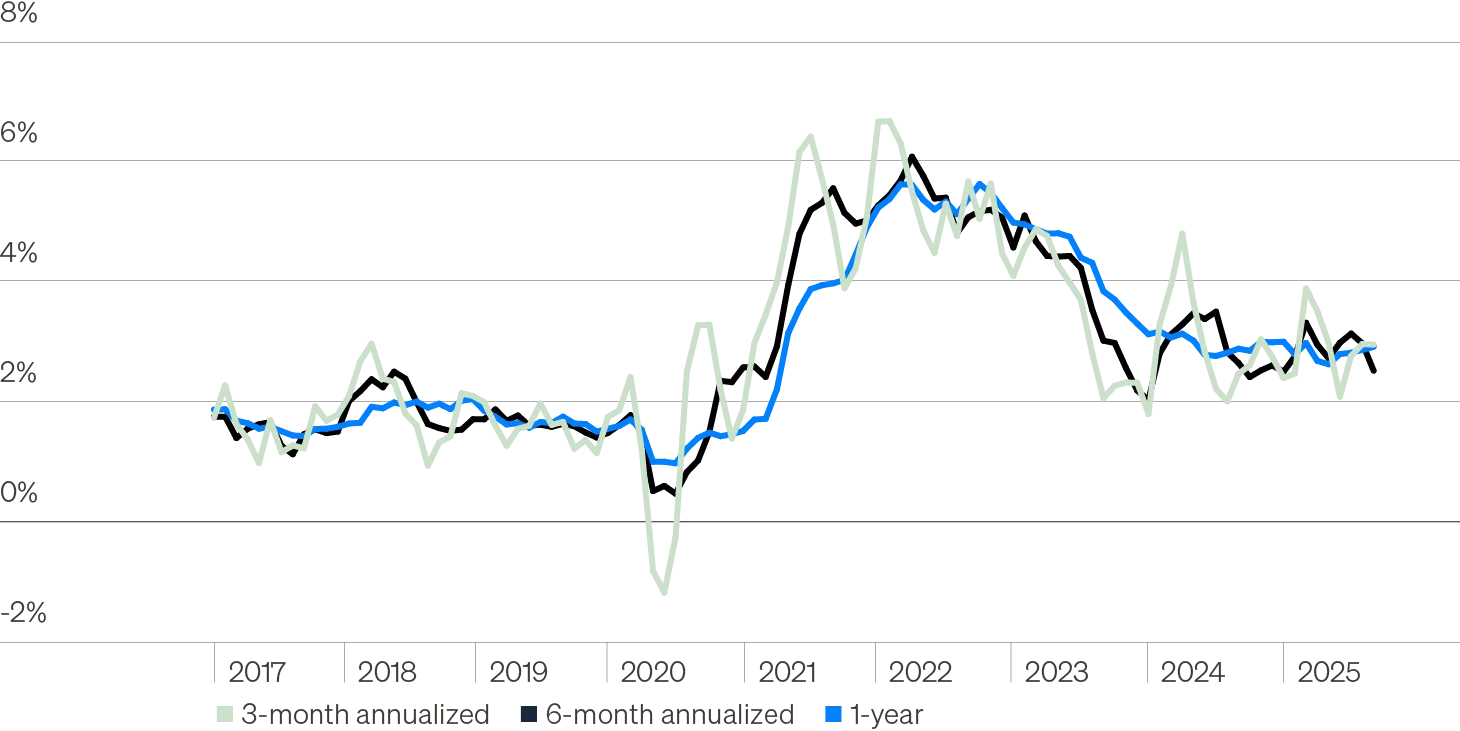

Inflation: Forgotten but not gone

Inflation remains central to the outlook for the U.S. economy, even if the Federal Reserve has pivoted its gaze to labor markets for the time being. While there have been ebbs and flows and shifts in the composition of price growth, there has been very little (if any) progress on inflation since the end of 2023.

Core PCE price index annualized changes using different periodicities

Get our outlook for the economy in Q4, what’s next for asset classes across public and private markets and what these trends mean for investors.